Money money money

I’ve been busy with some personal stuff lately, so less active on the blog than I like. Things are settling down, though, and I hope to return to my weekly-or-so cadence here.

There’s been plenty of action in the last couple of weeks — more legal residents disappeared, tariffs that led to a stock market rout, nationwide protests signaling, maybe, swelling dissatisfaction with the policies and practices of the Trump administration. There’s been good coverage of all that in the blogosphere and broader media. I won’t add to the outrage. I share it, but have nothing much new to offer.

Instead, I want to talk about banking. I aim, in the next few days, to talk about how to pay for the government we want. On the way there, though, it's useful to understand how the global and US financial systems operate. This longish explainer does that. If you know the names of three members of the Federal Open Market Committee, you can safely skip this one.

What is money?

Money is super interesting!

We’re not quite sure how it got invented. Did some clever trader dream up a lubricant for the barter system? Did matriarchs keep track of gifts and favors in villages, and come up with credit and debt? At some point, beads and rocks and coins and silver and gold became mediums of exchange. Those morphed over time into banknotes, and banknotes drifted from any direct relationship to beads and rocks and silver and (thanks to the Bretton Woods agreement after World War II) gold.

One useful way to think of money today is that it’s a consensual hallucination: We all agree that money has value because we all agree that money has value. I'm willing to trade you my used car for your envelope full of Benjamins or some electronic numbers from your Venmo account because I'm pretty sure other people will accept them from me for things that I want.

The United States is an important source of confidence for that belief. For centuries, the full faith and credit of the US has assured markets that America will make good on its bills. Other governments offer similar assurances, of course, but as the world’s reserve currency, the dollar and the US' guarantees are linchpins of the financial system and the confidence that it is built upon.

What banks do

Most folks have checking or savings accounts at banks. They deposit money in their accounts, and the bank promises to give it back to them when they want it. This practice is called borrowing short: The bank essentially borrows your money, maybe pays you a bit of interest, but is on the hook to return it at any time.

Banks take your checking and savings deposits, and mine, and those of all their other customers, pool them up and use them to lend money to other people. The banks charge those people a higher interest rate than they pay you for your savings, so they make a profit. This is how business loans and home mortgages are made. Banks lend long, paying out some of our deposits to people they think will pay it back on long-term, fixed payment schedules.

When a bank borrows short and lends long, it literally creates new money. You deposit $1000 in your savings account, and the bank lends $200 of that (and collects $200 from five other depositors!) to make a $1000 loan to your neighbor. Your neighbor deposits that $1000 in her bank account. Your money was multiplied – there are more dollars on deposit now than before the bank made the loan!

This is called fractional reserve banking. The banks take everyone's deposits in, but they only hold onto a fraction of those dollars. They use the rest to make loans. This is the primary social and economic value that banks provide: They take risks to facilitate economic growth and liquidity.

Of course, if every depositor at a bank demanded their money back at the same time, the bank would be in trouble. This used to happen with some frequency – it's called a bank run – and it often led to real losses for depositors. Over time, we've built up regulatory frameworks and agencies, as well as government guarantees, that sharply reduce the risk of loss. The taxpayer-backed Federal Deposit Insurance Corporation, or FDIC, for example, promises to step in to make depositors whole (up to a limit) in case a bank can't meet withdrawal demands. That assurance generally prevents bank runs altogether, because once a depositor is sure his money is safe, there's no reason to take it out of the bank.

The Federal Reserve and the US Treasury

You and I keep our money at commercial banks. There's another important kind of bank, though – the central bank – that plays a critical role in the economy, managing the money supply and working to keep inflation and unemployment at acceptable levels. Most countries have a central bank.

In the US, the central bank is called the Federal Reserve. It operates twelve regional banks in cities like Minneapolis and San Francisco. They work together to manage the US economy generally.

The Federal Reserve is able to create money in a different way from commercial banks.

The US Treasury issues bonds and other financial instruments that investors can buy. These instruments (there are different kinds, but I'll just use "bond" for simplicity) offer a fixed interest payment over some time period. At the end of that period, the US Treasury repays the invested amount in full. Treasury bonds are the way that the US is able to borrow money.

The Federal Reserve has a special power not available to any other bank. It can accept newly-created bonds from the US Treasury and conjure dollars (in digital form; we don't print paper currency for this purpose) out of thin air to pay for them. Economists call this quantitative easing.

If you are familiar with the accounting notion of a balance sheet, the Fed gets a free asset (a Treasury bond). It uses that asset to create dollars (called bank reserves) that it distributes to commercial banks. The reserves it created are a liability to the Fed (it has to make good on the dollars), but the liability is backed by a perfectly good Treasury bond, thanks to the "full faith and credit" doctrine.

The commercial banks can use the dollars they get to make loans to businesses or consumers.

The Fed generally uses this power only in times of economic trouble. Passing out free money isn't necessary when the economy is running well. During the 2008 subprime mortgage crisis, though, the Fed used exactly this mechanism to bail out banks. The banks used the free money to pay off losses that might have bankrupted them otherwise. During COVID, the checks that people received directly and the money used to fund the Payroll Protection Program, among other programs, was created like this.

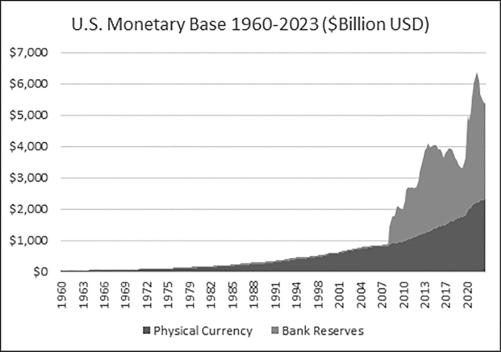

This is an expansion in the base money supply. Before the Federal Reserve did its magic trick, there were a certain amount of hard dollars in circulation; afterward, there were more. That expansion is generally inflationary, because there are now more dollars chasing the same amount of goods and services, so people who want those things will be willing and able to pay more for them, thanks to the extra dollars all over the place.

You can see the subprime crisis and COVID in the chart above, taken from chapter 15 of Lyn Alden's excellent book Broken Money. That lighter-grey surge of new dollars is due to quantitative easing, and is the reason for persistent inflation over the period.

You can see, too, in that graph that the bulge of new dollars – the lighter-grey blob – shrinks sometimes, too. In those cases, the Federal Reserve collects money from taxes or Payroll Protection Play repayments or whatever. It wipes out an equal value of the reserves that it has created, basically disappearing the dollars it created back into thin air. Economists call this quantitative tightening. Just as quantitative easing is generally inflationary, quantitative tightening is deflationary. Fewer dollars are chasing the same amount of goods and services.

Deficit financing

Conjuring money out of thin air via quantitative easing is a new-fangled way of debasing coinage or Germany's maniacal printing paper currency during World War II. You need computers for QE, but rulers have been doing it for as long as they've been in charge of the money supply.

There's a simpler way to use Treasuries, though.

A key job for the US Congress is to decide how much money to spend and what to spend it on. Mostly, it does that. Sometimes the whole Congress can't come to an agreement on a new budget. Mostly, when that happens, it agrees on a continuing resolution to keep spending as much as it has, in the same ways as before, until it can come up with a new plan.

The Congress also decides on tax rates and exemptions. That means it controls how much money the government takes in.

A simple way to run the country would be to make sure that the amount of money coming in every year from taxes and other sources matches the amount spent programs and services.

That's not always a good idea, though. In times of economic crisis, pandemic or war, it may make sense to borrow money to fund unusual programs. The "full faith and credit" doctrine has given the United States the ability to raise money on inexpensive terms. Doing so wisely allows us to meet unexpected challenges. There's even an economic argument that the US ought to use debt for domestic and global strategic reasons – investors, borrowers and lenders can be valuable geopolitical partners.

In general, though, the country has spent more than it takes in pretty consistently since 1980. Federal Reserve economic data shows a curve that moves mostly up over that period. It's not uniform; the country ran a budget surplus during Bill Clinton's administration and Joe Biden retired better than half the spike in debt incurred by COVID. As a percentage of GDP, though, our debt has quadrupled over four decades.

When Congress spends more money than the tax laws bring in, the government makes up the difference by selling Treasuries. Recall that investors buy those because they pay interest every year (so we have to spend money on an ongoing basis to pay for previous years' spending) and because they'll get paid out in full when the mature (so we have to pay a big chunk for every Treasury that matures in a given year). Of course, one way to pay interest and principal is to sell new Treasuries – to use new debt to pay off our old debts.

The politics of the US national debt

Legislators like quantitative easing and deficit spending. It's nice to be able to spend money!

There's a historical quirk in the US called the debt ceiling that limits how much the US government is allowed to owe. It was created to manage the sale of bonds that funded World War I and has survived to the present day. When the national debt gets close to the debt ceiling, the Congress has to vote to raise it. That's a fraught vote, when it happens. Occasionally, the Congress fails to raise the debt ceiling, and the Federal government is forced to shut down because it can't borrow any more. Some essential workers, like the branches of the military, must continue to work without pay, but most government workers are furloughed.

Public frustration eventually forces Congress to end a shutdown by raising the debt ceiling after all.

Voters strongly dislike taxes. They claim to dislike deficits as well, but they've been returning the same Senators and Representatives to Congress for many years. We tolerate debt, and increases in the debt ceiling, without exacting any real price from the legislators that vote for deficits.

The lesson for a Congressperson who aims to remain in Congress is that it's much safer to vote for quantitative easing, deficit spending and increases in the debt ceiling than for taxes or spending cuts.